Perhaps no word could make me cringe more in recent years than the one that had come to define this recent period of startup euphoria: Unicorn.

The term may have been briefly useful, back when one or two private companies exceeded $1 billion in valuation on paper a few years ago. But, as with so many things in the tech world, the industry has a way of taking a moderately interesting concept and running completely amok with it.

[aditude-amp id="flyingcarpet" targeting='{"env":"staging","page_type":"article","post_id":2138569,"post_type":"analysis","post_chan":"none","tags":null,"ai":false,"category":"none","all_categories":"business,","session":"C"}']When it seems every startup is a unicorn (or at least 183 of them by CB Insight’s current count), they are no longer what you could call rare creature. The word has become meaningless.

To be sure, it pointed to some underlying trends worth understanding better. Venture Capital was evolving, and more gigantic rounds of late-stage founding from non-traditional investors were allowing companies to stay private longer. The companies themselves wanted to avoid the scrutiny that came with being public and were happy to strike these deals.

AI Weekly

The must-read newsletter for AI and Big Data industry written by Khari Johnson, Kyle Wiggers, and Seth Colaner.

Included with VentureBeat Insider and VentureBeat VIP memberships.

But in truth, it seemed the idea of being a unicorn had taken on a marketing-driven meaning and become a way to create the appearance of momentum and success. It was a club that everyone wanted to join, and so valuations became the thing companies would lead with in press releases and marketing material, even though the variables that went into assessing such a number remained unverifiable.

This past year, thankfully, it seems that the appeal of being a unicorn has all but died.

I noticed this at the Web Summit in Lisbon back in November, where, except for a couple of nods here and there, it was rare to find anyone utter the word or include it in the name of a session.

Does calling your company #unicorn gives you more chance of becoming one? #websummit pic.twitter.com/sYDQuADeKr

— Gabriel Jarrosson (@GJarrosson) November 10, 2016

And the numbers bear this out.

According to CB Insights, the number of new unicorns created in 2016 dropped dramatically. CB Insights tracked 23 new unicorns in 2014 and 40 in 2015, based on valuations of rounds raised in those years. But there were only 12 new unicorns in 2016.

[aditude-amp id="medium1" targeting='{"env":"staging","page_type":"article","post_id":2138569,"post_type":"analysis","post_chan":"none","tags":null,"ai":false,"category":"none","all_categories":"business,","session":"C"}']

In part, that’s because the number of venture capital rounds over $100 million fell from 77 in 2015 to 41 in 2016. It seems that venture capitalists have grown tired of underwriting mega-startups and are looking for the exits.

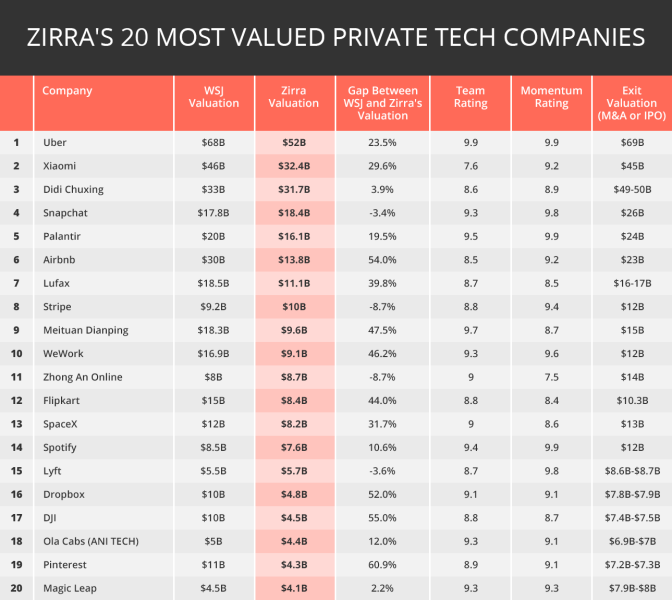

The problem, in the short-term, is that many companies will likely still be suffering a unicorn hangover entering 2017. Consider a recent analysis from Zirra, a company that has developed a new method for analyzing private company valuations using AI and machine learning. Zirra says it uses a combination of 85 licenses and publicly available databases to calculate revenue, expense estimates, investment history, and other metrics, and then compares those to a large database of competitors.

Comparing its own calculations to the Wall Street Journal‘s list of publicly reported private valuations, Zirra estimates that the top 20 unicorns are overvalued by 26.5 percent. The most overvalued unicorns, according to Zirra, include:

[aditude-amp id="medium2" targeting='{"env":"staging","page_type":"article","post_id":2138569,"post_type":"analysis","post_chan":"none","tags":null,"ai":false,"category":"none","all_categories":"business,","session":"C"}']

- Xiaomi: 29.6 percent gap — Zirra values at $32.4 billion; WSJ values at $46 billion

- Airbnb: 54 percent gap — Zirra values at $13.8 billion; WSJ values at $30 billion

- WeWork: 46.2 percent gap — Zirra values at $9.1 billion; WSJ at $16.9 billion

- SpaceX: 31.7 percent gap — Zirra values at $8.2 billion; WSJ at $12 billion

- Dropbox: 52 percent gap — Zirra values at $4.8 billion; WSJ at $10 billion

- Pinterest: 60.9 percent gap — Zirra values at $4.3 billion; WSJ at $11 billion

Here is the full list published by Zirra:

If Zirra’s analysis is correct, many of these companies have painted themselves into a financial corner. In terms of either an IPO or an acquisition, they may have difficulty achieving an exit that comes anywhere close to their most recent fundraising valuation. And if they need to raise more money, a so-called “down round” is likely, in which case the company is going to be facing a negative swirl of publicity that could impact its ability to hire.

Of course, it’s possible that the publicly reported valuations listed by the WSJ were mostly phony, in which case these companies may be just fine as far as their investors are concerned.

[aditude-amp id="medium3" targeting='{"env":"staging","page_type":"article","post_id":2138569,"post_type":"analysis","post_chan":"none","tags":null,"ai":false,"category":"none","all_categories":"business,","session":"C"}']

Still, it seems clear that 2016 taught many companies that being a unicorn was not nearly as glamorous as it appeared to be. In 2017, we may find out just how painful and costly that lesson will turn out to be for the most overvalued startups in the herd.

VentureBeat's mission is to be a digital town square for technical decision-makers to gain knowledge about transformative enterprise technology and transact. Learn More