Above: An orchestra played video game music on day two of MIGS 15.

GamesBeat: What else can a company do to make itself more investor-ready?

Alloul: Most people underestimate the impact that—The material that you have to produce shouldn’t cross the line of sitting in front of GS, sitting in front of a potential bank—It’s the readiness of the material you have to produce. Some people say, “Eh, I’ll deal with that later, I’ll hire an accountant.” That will cost you a lot. You’ll have one week to produce this material and you’re not ready. That lack of preparation can cost you 20 or 30 percent of your valuation, if you aren’t simply rejected outright.

That’s one reason why I founded a company called Budgeto that isn’t focused on games. It’s a budget tool that helps entrepreneurs create an online budgeting model in a couple of hours, so they can be ready to talk in front of a bank.

Della Rocca: It’s a whole day-long workshop to prep for this kind of stuff. Doing the due diligence, or what we call a day room, and having that day room ready to go in terms of all your budgets and forecasts and key documents and contracts and so on. We often do a due diligence type of presentation, and it’s extensive. A lot of developers don’t tie the knots on all their legal elements. They don’t have contracts with their employees. They don’t have their minute books ready.

One of the most important things is the chain of IP. You want to make sure that if you’re using your buddies and freelancers and other indies pitching in, they’ve signed proper contracts and signed their IP over to the project and the company. Even if they’re doing it for free, they have to formally sign over the IP. If you’re talking to a publisher or investor or bank and you have all these loose relationships with people pitching in, that’s a massive red flag.

There’s a whole bunch of other stuff related to how a company’s structured, the partnerships between the co-founders, that may prevent or make it complicated for investors to come in. Again, there’s probably too much detail to get into here, but all comes back to the notion of being investable. It’s one thing to say, “I need money and what I’m doing is cool.” There are situations where the things you’re doing actively thwart the ability of people to give you money, because you don’t know any better or you haven’t talked to the right lawyers or accountants and stuff. Getting that kind of professional help really does facilitate things if you’re chasing investment. It’s super critical to be investable.

Another one, just on the planning side, it’s amazing how many studios pitch to us and—They’re very focused on how awesome their gameplay is, or their art. They’re developers, so they’re very passionate about what they do. But they haven’t thought through the market potential. They haven’t fully articulated what their audience is, where it is, how they’ll find it, and how they’ll beat their competitors to get those users to buy their game.

Often they don’t even do forecasts on what they think the upward potential is. They come to us and say they need, whatever, a million-dollar budget. Okay, how many units do you think you’ll sell? We’ll have a conversation and realize that maybe they won’t even make $1.2 million. The math just doesn’t work. Of course a lot of that is speculation. You can’t guarantee how many units you’ll move. But if you’re not estimating or even thinking about what the potential is, it just doesn’t make sense. Why should an investor take that risk?

Cournoyer: Another way to look at it is, instead of looking at yourself as a game studio, look at yourself as a startup. There are reams of information about how to position yourself as a startup and get in front of investors. Thousands of blogs you can read. A lot of information is out there. Look at your project as a startup and do an investor pitch that’s built the way a startup would build one. That’s a good way to look at it.

Zhu: I agree with what Jason’s saying. At CMGE We provide different options in terms of investment, whether it’s strategic investment or project funding. But our preference goes toward strategic, active investment on top of a publishing deal. If we sign a publishing deal for a game title, that’ll be a very good test of a studio’s capability. We can see the market reaction to the game in terms of revenue, userbase, and KPIs.

Alloul: As an investor we know that the data you’re going to present will not be perfectly accurate. What we’re going to look at is the methodology of thinking behind your data. You need to be prepared with a worst-case scenario, a base scenario, an optimistic scenario. Back up your data. What’s your burn rate for 12 months? How are you going to ramp up?

If you’re calculating a tax credit here in Canada, it has to be properly documented. If you’re thinking the tax credit comes in the year when you apply, that’s one of the most common mistakes people make. “We only need $500K because we’ll get a $250K tax credit.” No, because you won’t get the credit for 18 months.

Whether you apply to raise a debt of $25,000, liquid investing of $50,000, early stage investing of $250,000, or in our case we invest $2-5 million, the due diligence will be the same process. You’ll be asked for the same documentation along the way. Maybe less at an early stage, but it’ll be the same packaging. The earlier you’re ready, the better your chances.

We’re asking more and more from entrepreneurs. It used to be that you just had to be a passionate, creative game developer. Now you have to understand legal and financial issues. It’s tough to be an entrepreneur.

Question: Along the lines of machine learning and algorithmic game creation, at the end of the day we’re making cultural content. In Canada, we’re making something that exports our view of what the world is like in the form of a game. I’m concerned that when game companies are entirely viewed as startups, we miss something essential in how we value that quality. Can you respond to the notion of how much you attribute to the creative value of a game in your overall valuation?

Della Rocca: The reality is, despite the fact that we’ve been talking a lot about spreadsheets and due diligence and legal issues and so on, I will not touch a game that isn’t interesting, creative, innovative, that features some kind of meaningful design. I’m not looking for Candy Crush clones because we think the spreadsheet comes out nicely.

From Execution Labs’ perspective, we’re looking for developers who are talented and passionate, who believe in what they’re doing as a medium. They’re creating something with some kind of meaning or innovation, but doing that in the context of commercial intent. They’re building this with an audience in mind. They’re going to deliver it to that audience and make money. Whether or not they eventually make money, at least they have the intent. That’s the goal.

At the same time, there are other venues and elements and platforms in the game industry where if you just want to be a starving artist punk rocker, you have the opportunities to create and express yourself in the same way that music or dance or film—Not all of it is encapsulated in an investable industry. It’s an art form. In the sense that you’re trying to build a business and take other people’s money to grow that business, it has to be done in the context of commercial intent. But we do so with games that have some kind of meaning or vision.

Above: Ubisoft’s For Honor tournament at MIGS 15.

Cournoyer: If you look at very successful startups, they’re created by entrepreneurs who are passionate about what they’re doing. They’re passionate about a problem they’re experiencing and they want to solve, or they’re passionate about this new thing they invented. They use a company as a way to take that innovation or the solution to that problem to the world.

If you make a parallel to the game industry, you start with a game you want to build. That game is the creative piece. It’s the art. But the mechanics and the process by which you will build that business around that game, that’s where I see machine learning being applied. Not in the emotion you want to convey with the game, because that’s where it starts. It starts with the emotion you want players to feel when they’re playing. But then it’s in how you’ll take this initial vision and have it evolve so it becomes a sustainable, financially successful long-term business.

Zhu: The cultural element can a very broad topic. A specific cultural orientation can be a pro or a con. But my opinion is that good game or a movie or anything else can be taken worldwide. I’ve seen lots of games in test-build form from Canada and the U.S. and Europe. Some developers don’t produce games for money. They make games for themselves. And our preference, unfortunately, isn’t to publish that kind of game. We go for profit.

Question: I’d like to understand what your goals are when you invest in startups, and video game companies specifically. What’s your ideal exit? What kind of return would you like on your investment, and in what time period? What’s your goal?

Della Rocca: Understanding that as an entrepreneur is part of the process of knowing who it is you’re pitching to. It’s the start of that bartering process. The reality is that the answer is different for everyone. A seed stage investor is looking for a different type of return from an angel investor, who’s looking for something personal to get behind. They want to lend their knowledge as well as earn a return. A later-stage growth VC is writing very big checks and the ROI is very different. You’ll get different answers from each of us and every investor you talk to.

Oftentimes the more strategic the investor, the less pressure there is on the economic side. They’re investing in you because they see you plugging in a talent or IP. They see some value in you that’s not purely economic. They may want you to make money as well, but it’s more about these other things. That will change depending on who the strategic investor is, though. The more banker side, it’s literally, “I give you money, and in five years you give that money back, plus some more.” It’s quite a broad range of demands.

Generally speaking, if possible, you want to tend toward the more strategic side of the spectrum. That often means you’re getting something of non-economic value as well. Let’s say it’s a publisher. You’re getting access to marketing as well. You’re not just getting a check to fund your development.

We’re almost a pre-seed investor. We’re investing at a very early stage. We’re investing, as I mentioned, on a longer-term horizon. We want you to be making games and building momentum on a longer-term basis. If there’s an exit possible, where Microsoft comes in and buys you like the next Mojang, that’s great, because we do take an equity percentage. But we also have a trigger that asks you to buy back the shares from us if you’ve been profitable and have cash on hand. If you’re doing well as a company, but Microsoft isn’t coming to buy you for $2 billion, that allows us to exit at a fair market valuation.

In that sense, while we’re working with studios to help them become as successful as possible, some might be more on that “get bought for $2 billion” path, and some others might not want to ever reach that. But we’re able to have a diversity of exits or dividends and so on. The economics of a pure VC are much different.

Cournoyer: We typically take a 10 or 15 percent ownership stake in the companies we invest in. We look to invest in projects where, assuming everything goes well, in a positive outcome, we as a fund make $15 to $20 million. You’re looking at a couple hundred million per exit, is the target we go for.

Alloul: W Investment was initially a fund investing in early stage companies. At that level you’d better already have $15 or $20 million in your pocket before you start to play. Statistically speaking, we looked at the results we had and came to the conclusion that you’re going to lose some or win some. You’re hoping that the exit brings you 20, 30, 50 times your investment.

We modified that thinking, which is why we created W2 and W3 Investments. We sacrificed the multiple we’re looking for against some risk tolerance. That’s why we now invest only in companies that have existing revenue and profitability, that are cash-flow positive or about to be. Because we’re investing a greater amount — $2-5 million – we’re not dreaming of 20. We’re happy if we do five, three, six, whatever it is. It’s more important for us to not lose our money, as opposed to dreaming of making 50 times our money.

The big difference is that in some cases, the investors are investing someone else’s money. That’s why, to Jason’s point, you have to understand who you’re sitting down with. Are you talking to investors from the government, institutional investors, banks? In our case this is a private fund, which means we have no limited partners. This is our own money. That’s why we’re very cautious.

Above: An exhibit of motion capture and VR at the MIGS 15 event in Montreal.

Question: Early on you mentioned you invested in Retinad. That seems like a riskier action than what you’re talking about there.

Alloul: That’s a good point. The investment in Retinad is a lot less money than we normally do. We’ll do maybe one deal a year, two deals a year, that are more because we know the entrepreneurs, and so we’ll do something outside our normal focus. It’s a very small amount in that case.

Question: Do you believe that it’s hard and fast rule that mobile developers need to keep creating more content post-launch to maintain retention for their games? Or do you think that games still have the ability to sell themselves as a self-contained package? Is there ever a boundary where those design decisions are more or less acceptable in the eyes of an investor?

Della Rocca: To me, additional content is about retention and engagement of your existing players. You do enough content to acquire users and get them involved in your product, but then at some point your retention will drop dramatically if you don’t have any new content for them. Unless it’s more of a multiplayer game, like Clash of Clans, where just playing against other players is what brings people back to the game.

Cournoyer: I don’t know if you’re asking that question more in the context of paid or freemium games, but to echo Jason’s point, you need to do whatever is necessary to retain and engage your users. In certain games that’s adding content. In other games that’s not as necessary.

On the mobile side the bigger challenge is user acquisition to begin with. Creating new content can also be part of the acquisition process, but the bigger problem is developers who think they can make their awesome little game, put it on the app stores, charge a buck or two, and players will come to them. That just doesn’t happen anymore, or only in very rare cases.

In building a game as a service you have to be thinking about the user funnel of acquisition, retention, engagement, conversion, and so on. You have to be engaging with players that have deep pockets for user acquisition – publishers, strategic investors, or if the metrics look really good, VCs who may still come in. If you’re not building the game with that mind, you’re almost dead in the water these days.

Zhu: Additional content is very important to keep up retention and acquire new users. From our experience, we always want a developer to do fast iteration right after the launch of a game. They need to add new content constantly.

Della Rocca: If the game is not doing well, of course – if players are not coming back to the game, if they’re not being retained by what the game is fundamentally — adding new content is probably not going to result in success. You need to go back and look at the data and understand why players are dropping off before you just make content because it gives you the opportunity to make noise.

If the game is fundamentally working, then yes, adding new content to keep those players engaged over the longer term is usually a good strategy. But if the game isn’t working to begin with, you have other problems to solve before you start making new levels.

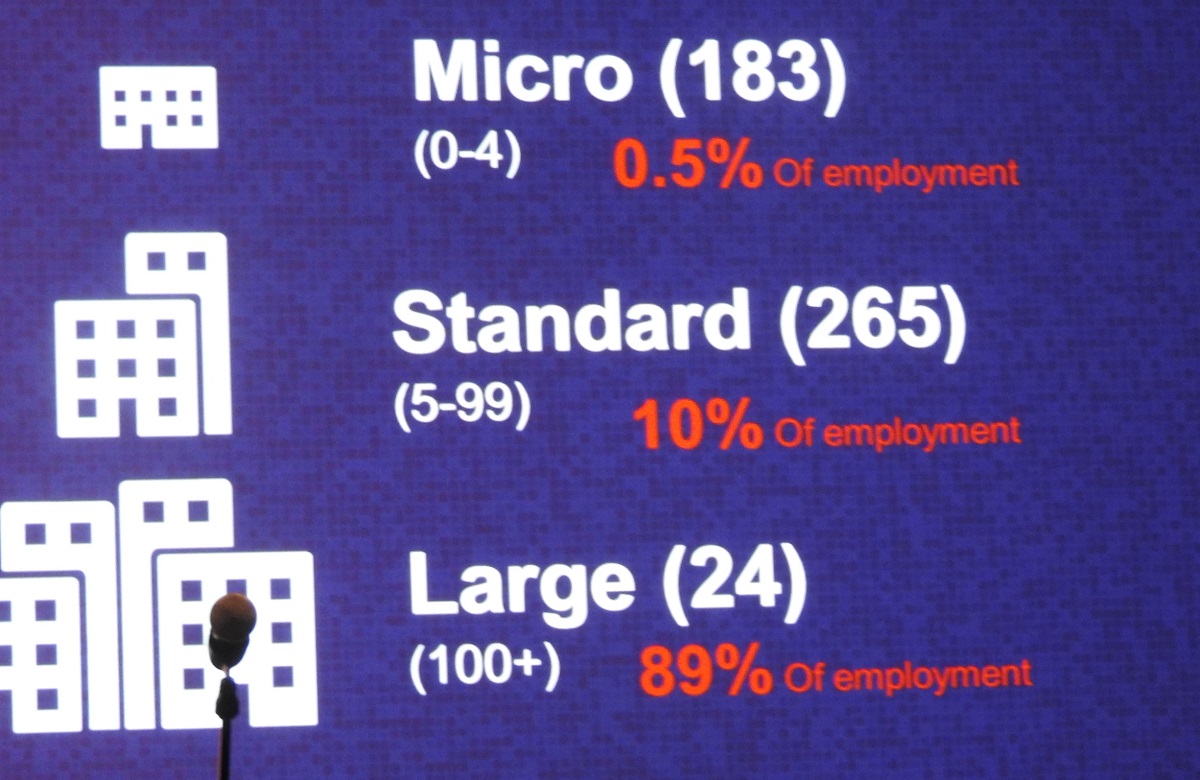

Above: Canada’s micro game studios are growing, but major companies employ most of its game developers.

VentureBeat's mission is to be a digital town square for technical decision-makers to gain knowledge about transformative enterprise technology and transact. Learn More