Want smarter insights in your inbox? Sign up for our weekly newsletters to get only what matters to enterprise AI, data, and security leaders. Subscribe Now

There are many reasons to found a startup — and many reasons to work at a startup. But there’s only one reason your company got funded: Liquidity.

The good news

To most founders a startup is not a job, but a calling.

But startups require money upfront for product development and later to scale. Traditional lenders (banks) think startups are too risky for a traditional bank loan. Luckily, in the last quarter of the 20th century, a new source of money called risk capital emerged. Risk capital takes equity (stock ownership) in your company instead of debt (loans) in exchange for cash.

Founders can now access the largest pool of risk capital that ever existed – in the form of private equity (angel investors, family offices, venture capitalists, and hedge funds).

At its core, venture capital is nothing more than a small portion of the private equity financial asset class. But for the last 40 years, it has provided the financial fuel for a revolution in life sciences and IT and has helped to change the world.

The bad news

While startups are driven by their founders’ passion for creating something new, startup investors have a much different agenda: a return on their investment. And not just any return. VCs expect large returns. VCs raise money from their investors (limited partners like pension funds) and then spread their risk by investing in a number of startups (called a portfolio). In exchange for the limited partners tying up capital for long periods by in investing in VCs (who are investing in risky startups,) the VCs promise the limited partners large returns that are unavailable from most every other form of investment.

Some quick VC math: If a VC invests in 10 early stage startups, on average, five will fail, three will return capital, and one or two will be “winners” and make most of the money for the VC fund. A minimum “respectable” return for a VC fund is 20% per year, so a 10-year VC fund needs to return six times (6x) its investment. This means that those two winner investments have to make a 30x return to provide the venture capital fund a 20% compound return – and that’s just to generate a minimum respectable return.

(By the way, angel investors do not have limited partners, and often invest for reasons other than just for financial gain — such as helping pioneers succeed — and so the returns they’re looking for may be lower.)

The deal with the devil

What does this mean for startup founders? If you’re a founder, you need to be able to go up to a whiteboard and diagram out how your investors will make money in your startup.

While you might be interested in building a company that changes the world, regardless of how long it takes, your investors are interested in funding a company that changes the world so they can have a liquidity event within the life of their fund ~7-10 years. (A liquidity event means that the equity — the stock — you sold your investor can now be converted into cash.) This happens when you either sell your company (M&A) or go public (an IPO). Currently, M&A is the most likely way for a startup to achieve liquidity.

Know the end from the beginning

Here’s the thing most founders miss: You’ve been funded to get to a liquidity event. Period. Your VCs know this, and you need to know this too.

Why don’t VCs tell founders this fact? For the first few years, your VCs want you to keep your head down, build the product, find product/market fit, and ship to get to some inflection point (revenue, users, etc.). As the company goes from searching for a business model to growth, only then will they bring in a new “professional” management team to scale the company (along with a business development executive to search for an acquirer) or prepare for an IPO.

The problem is that this “don’t worry your little head” strategy may have made sense when founders were just technologists and the strategy and tactics of liquidity and exits were closely held, but this is a pretty dumb approach in the 21st century. As a founder you are more than capable of adding value to the search for the liquidity event.

Therefore, founders, you need to be planning your exit the day you get funded. Not for some short-time “lets flip the company” strategy; you need to have an eye on who, how, and when you can make an acquisition happen.

Step 1: Figure out how your startup generates value. For example, in your industry, do companies build value the old fashioned way by generating revenue? (Square, Uber, Palantir, Fitbit, etc.) If so, how is the revenue measured? (Bookings, recurring revenue, lifetime value?) Is your value to an acquirer going to be measured as a multiple of your revenues? Or, as with consumer deals, is the value ascribed by the market?

Or do you build value by acquiring users and figuring out how to make money later (WhatsApp, Twitter, etc.) Is your value to an acquirer measured by your number of users? If so, how are the users measured (active users, month-on-month growth, churn)?

Or is your value going to be measured by some known inflection point? First-in-human proof of efficacy? Successful clinical trials? FDA approvals? CMS reimbursement?

If you’re using the business model canvas, you’ve already figured this out when you articulated your revenue streams and noted where they are coming from.

Confirm that your view of how you’ll create value is shared by your investors and your board.

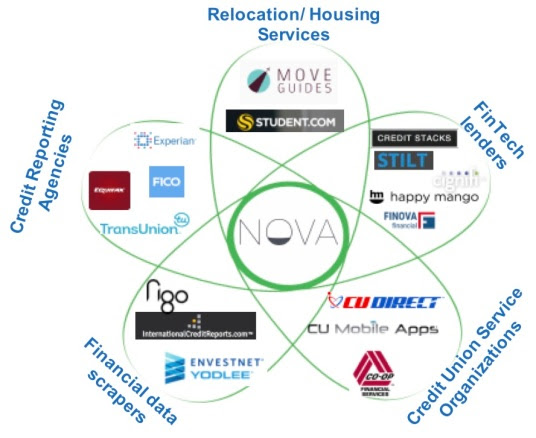

Step 2: Figure out who are the likely acquirers. If you are building autonomous-driving aftermarket devices for cars, you can make a shortlist of potential acquirers – auto companies and their tier-one suppliers. If you’re building enterprise software, the list may be larger. If you’re building medical devices, the list may be much smaller. But every startup can take a good first cut at a list. (It’s helpful to also diagram out the acquirers in a Petal Diagram). When you do, start a spreadsheet and list the companies. (As you get to know your industry and ecosystem, the list will change.)

Step 2: Figure out who are the likely acquirers. If you are building autonomous-driving aftermarket devices for cars, you can make a shortlist of potential acquirers – auto companies and their tier-one suppliers. If you’re building enterprise software, the list may be larger. If you’re building medical devices, the list may be much smaller. But every startup can take a good first cut at a list. (It’s helpful to also diagram out the acquirers in a Petal Diagram). When you do, start a spreadsheet and list the companies. (As you get to know your industry and ecosystem, the list will change.)

It’s likely that your investors also have insights and opinions. Check in with them as well.

Step 3: List the names of the business development, technology scouts, and other people involved in acquisitions and note their names next to the name of the target company.

All large companies employ people whose job it is to spot and track new technology and innovation and follow its progress. The odds on day-one are that you can’t name anyone. How will you figure this out? Congratulations, welcome to Customer Discovery.

- Treat potential acquirers like a customer segment. Talk to them. They’re happy to tell anyone who will listen what they are looking for and what they need to see by way of data or otherwise for something to rise to the level of seriousness on the scale of acquisition possibilities.

- Understand who the Key Opinion Leaders in your industry are and specifically who acquirers assemble to advise them on technology and innovation in their areas of interest.

- Get out of the building and talk to other startup CEOs who were acquired in your industry. How did it happen? Who were the players?

It’s common for your investors to have personal contacts with business development and technology scouts from specific companies. Unfortunately, it’s the rare VC who has already built an acquisition roadmap. You’re going to build one for them.

It’s common for your investors to have personal contacts with business development and technology scouts from specific companies. Unfortunately, it’s the rare VC who has already built an acquisition roadmap. You’re going to build one for them.

After a while, you ought to be able to go to the whiteboard and diagram the acquisition decision process much like a sales process. Draw the canonical model and then draw the actual process (with names and titles) for the top three likely acquirers.

Step 4: Generate the business case for the potential acquirer. Your job is to generate the business case for the potential acquirer; that is, to demonstrate with data produced from testing pivotal hypotheses why they need what you have to improve their business model (filling a product void; extending an existing line; opening a new market; blocking a competitor’s ability to compete effectively, etc.).

Step 5: Show up a lot and get noticed. Figure out what conferences and shows these acquirers attend. Understand what is it they read. Show up and be visible – as speakers on panels, accidentally running into them, getting introduced, etc. Get your company talked about in the blogs and newsletters they read. How do you know any of this? Again, this is basic Customer Discovery. Take a few out to lunch. Ask questions: What do they read? How do they notice new startups? Who tells them the type of companies to look for?

Step 6: Know the inflection points for an acquisition in your market. Timing is everything. Do you wait seven years until you’ve built enough revenue for a billion-dollar sale? Is the market for machine learning startups so hot that you can sell the company for hundreds of millions of dollars without shipping a product?

For example, in medical devices, the likely outcome is an acquisition way before you ship a product. Med-tech entrepreneurship has evolved to the point where each VC funding round signals that the company has completed a milestone – and each of these milestones represents an opportunity for an acquisition. For example, after a VC Series B round, an opportunity for an acquisition occurs when you’ve created a working product and you have started clinical trials and are working on getting a European CE mark to get approval.

When to sell or go public is a real balancing act with your board. Some investor board members may want liquidity early to make the numbers look good for their fund, especially if it is a smaller fund or if you are at a later point in their fund life. If you’re on the right trajectory, larger funds or funds that are early in their fund life may be happy to wait years for the 30x or greater return. You need to have a finger on the pulse of your VCs and the market and to align interests and expectations to the greatest extent possible.

You also need to know whether you have any control over when a liquidity event occurs and who has to agree on it. (Check to see what rights your investors have in their investment documents.) Typically, a VC can force a sale — or even block one. Make sure your interests are aligned with your investors.

Part of the deal you signed with your investors was a term specifying the liquidation preference. The liquidation preference determines how the pie is split between you and your investors when there is a liquidity event. You may just be along for the ride.

Above all, don’t panic or demoralize your employees

The first rule of Fight Club is, you do not talk about Fight Club. The second rule of Fight Club is, you DO NOT talk about Fight Club! The same is true about liquidity. It’s detrimental to tell your employees who have bought into the vision, mission, and excitement of a startup to know that it’s for sale the day you start it. The party line is, “We’re building a company for long-term success.”

Do not obsess over liquidity

As a founder, there’s plenty on your plate – finding product/market fit, shipping product, getting customers, etc. Liquidity is not at the top of your list. Treat this as a background process. But thinking about it strategically will affect how you plan marketing communications, conferences, blogs, and your travel.

Remember, your goal is to create extraordinary products and services – and in exchange there’s a pot of gold at the end of the rainbow.

Lessons learned

To wrap it all up, here are the key things to remember:

- The minute you take money from someone, their business model becomes yours

- Your investors funded you for a liquidity event

- You need to know what “multiple” an investor will allow you to sell the company for

- Great entrepreneurs shoot for 20X

- You need at least a 5x return to generate rewards for investors and employee stock options

- A 2X return may wipe out the value of the employee stock options and founder shares

- You can plan for liquidity from day one

- Don’t demoralize your employees

- Don’t obsess over liquidity; treat it strategically

Steve Blank is a retired serial entrepreneur-turned-educator who has changed how startups are built and how entrepreneurship is taught. He created the Customer Development methodology that launched the lean startup movement, and wrote about the process in his first book, The Four Steps to the Epiphany. His second book, The Startup Owner’s Manual, is a step-by-step guide to building a successful company. Blank teaches the Customer Development methodology in his Lean LaunchPad classes at Stanford University, U.C. Berkeley, Columbia University, UCSF, NYU, the National Science Foundation and the I-Corps @NIH. He writes regularly about entrepreneurship at www.steveblank.com.