It was a year for the history books in games.

2014 saw a record $24 billion in game-company exits spread over both acquisitions and initial public offerings. Mobile drove more than half of all value that was created for management teams and early stage investors. For perspective, that’s the equivalent of about 10 Minecraft deals (at $2.5 billion, Microsoft’s purchase price for the block-building game’s developer, Mojang).

[aditude-amp id="flyingcarpet" targeting='{"env":"staging","page_type":"article","post_id":1645358,"post_type":"exclusive","post_chan":"none","tags":null,"ai":false,"category":"none","all_categories":"business,entrepreneur,games,mobile,","session":"D"}']More than $15 billion of the total came from acquisitions, and of that number, five megadeals accounted for $8.1 billion. Another $9 billion came from IPOs, which Asia dominated. You might think this is a bubble, but you would be wrong. Something more subtle is going on, and you can see it when you follow the money.

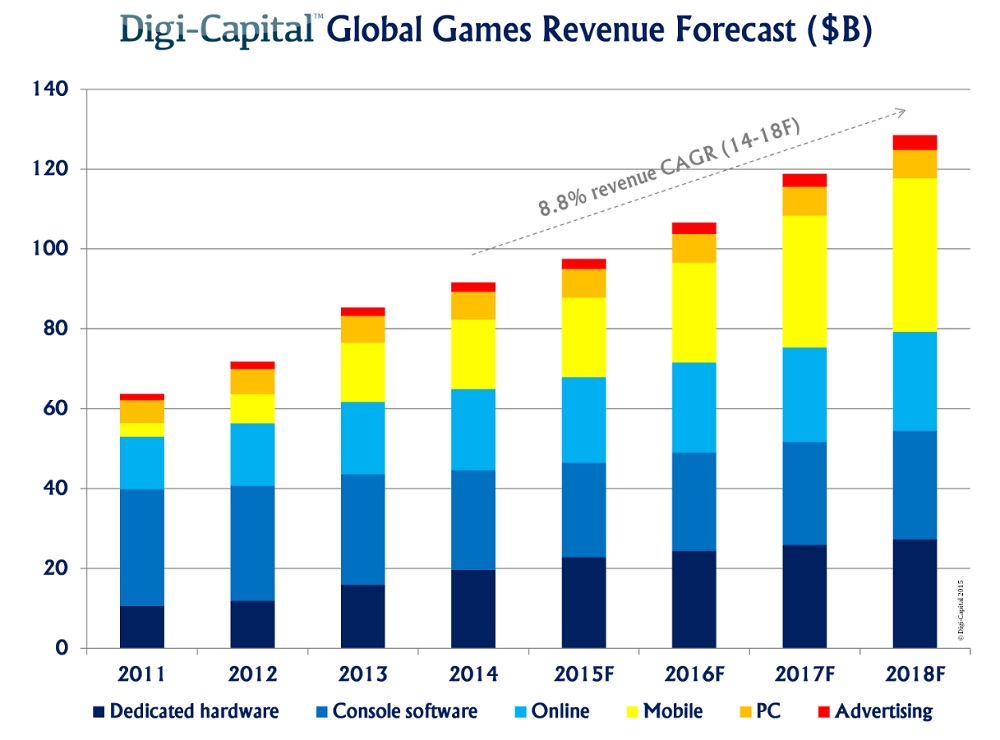

At the start of 2014, we forecast $100 billion games revenue (more, if you include hardware) by 2017. Other analysts followed with similar forecasts throughout the year. We were wrong.

AI Weekly

The must-read newsletter for AI and Big Data industry written by Khari Johnson, Kyle Wiggers, and Seth Colaner.

Included with VentureBeat Insider and VentureBeat VIP memberships.

Having tracked what’s happening across sectors through 2014 — from the go-go markets of Asian mobile games to the recovering Western console space — we’ve seen the nature of growth changing. It has stabilized. So while we still forecast games hitting $100 billion in revenue, we think it’s going to take another year to do it — not until the end of 2018. Mobile is the only sector showing strong double-digit growth, although virtual reality could become a breakout emerging platform. Asia is the No. 1 game market, set to hit $45 billion revenue in 2018 driven by China, Japan and South Korea. We forecast 8.8 percent compound annual growth rate (CAGR, an acronym for growth) for games software/hardware between 2014 and 2018. That sounds healthy, but it means single-digit growth. And that changes things. A lot.

Above: Global game revenue forecast

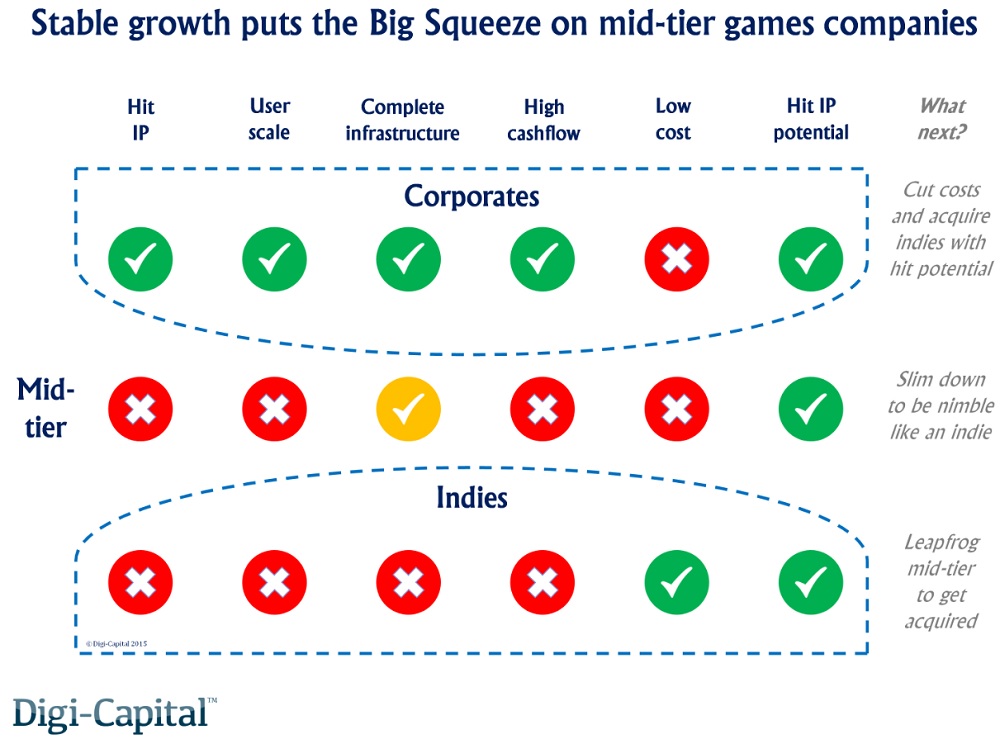

The big squeeze

In markets with single-digit growth, a rising tide no longer lifts all boats. Competition becomes about the difference between the great and the good.

In this phase of the market, big corporate entities with hit intellectual properties (IPs), massive user scale, and cashflow can invest in the high costs of marketing and infrastructure to compete in a stable growth market. This reduces everybody’s margins. Indies don’t have hit IPs yet or the scale advantages, but they don’t have the costs, either. Both can produce hit games, even if they are few and far between. Midtier game companies have no hit IPs yet, no scale advantages, but higher infrastructure and marketing costs. They can produce hit IPs too, but their cost bases increase their risk. They suffer from what what we call “The Big Squeeze.”

The other challenge for the midtier is the nature of acquisitions and investments in a stable growth market. Corporate buyers are managing their own cost bases and are less interested in team acquisitions. So the last thing they want is to buy someone else’s costs. Midtier game companies without major traction also struggle to raise money. Game investment grew to only $1.5 billion in 2014, a figure that is still 25 percent lower than in 2011.

It’s also hard to leapfrog the big guns in the mobile top 100. That’s why the market is putting the Big Squeeze on mid-tier games companies.

Above: Growth puts the big squeeze on midtier game makers.

Public game company stocks were broadly down 14 percent in 2014. But the big corporate buyers are managing their cost bases and looking to buy indies with unrealized hit potential to plug into their infrastructure and marketing. Or they will buy breakout companies with high-quality games (i.e., great ratings) and high downloads on mobile (or that can be adapted to mobile).

[aditude-amp id="medium1" targeting='{"env":"staging","page_type":"article","post_id":1645358,"post_type":"exclusive","post_chan":"none","tags":null,"ai":false,"category":"none","all_categories":"business,entrepreneur,games,mobile,","session":"D"}']

In that context America and China had the top 10 acquirers in 2014, and that’s where we still see demand. Indies are doing what indies have always done: try to bootstrap great games for fame and glory (and maybe get bought). The squeezed mid-tier now has a choice: become great and get bought, or slim down to become nimble like an indie and survive. Just being good is no longer good enough.

Until the next innovation wave accelerates market growth, consolidation rules. For everyone in the game industry, this is the time to become great.

Tim Merel is managing director of Digi-Capital, and this post is based on Digi-Capital’s new Global Games Investment Review 2015 at www.digi-capital.com/reports.

VentureBeat's mission is to be a digital town square for technical decision-makers to gain knowledge about transformative enterprise technology and transact. Learn More