Want smarter insights in your inbox? Sign up for our weekly newsletters to get only what matters to enterprise AI, data, and security leaders. Subscribe Now

The dust from last week’s abrupt shuttering of Mode Media — a company once valued at $1 billion and with $100 million in revenues — is anything but settled. According to a document obtained by VentureBeat, the company had access to $10 million in financing as recently as six months ago. Further, even as Hubert Burda Media, which had taken control of the company, said it had no option but to pursue a sudden shutdown, Mode’s Burda-controlled board had already decided to shut down the company one week earlier, VentureBeat has learned.

This pair of facts contradicts recent statements by Burda spokespeople and raises a series of questions about events that led to the September 15 closure of Mode. Left in the lurch are some 300 employees without access to basic benefits like COBRA insurance, thousands of publishers and bloggers to whom Mode owes revenue-share payments, investors who provided more than $225 million in funding, and a long line of creditors.

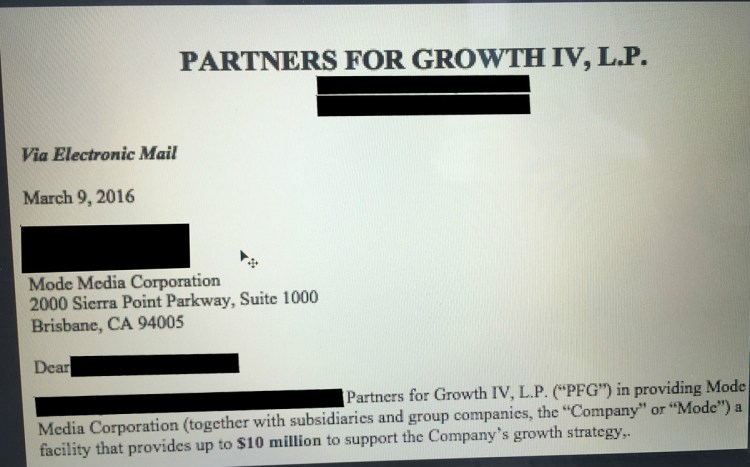

A leaked document obtained by VentureBeat shows a cover letter, dated March 9, of a $10 million financing term sheet from private equity firm Partners for Growth (see above). Yet earlier this week, a Burda spokesperson told The New York Post that “The board didn’t see any financial offerings.”

According to sources, the company had access to the PFG money, as shown on the March 9 letter, and final closing documents were delivered to the Mode board on April 1. One month prior, the board was presented a preliminary version of the term sheet and instructed company management to pursue this financing. PFG did not immediately respond to a request for comment.

When it came time to approve the PFG deal, directors Marc Andreessen, of Andreessen Horowitz; Samir Arora, cofounder and then-CEO; and Ernie Cicogna, then-CFO, voted in favor. Gary Efferen, a former media executive, supported the Burda directors in voting against. Andreessen subsequently resigned, and Efferen eventually left, as well. In April, Arora was replaced as CEO by longtime executive Jack Rotolo. Over the next few months, Burda effectively took control of the company’s board seats and, as the sources suggested, gained a majority of shares in the privately held corporation.

It’s unclear why Burda might claim that Mode was unable to get the external funding to continue operations, sell itself, or at least pursue an orderly closure. It’s possible that Burda hoped to fund the company itself, that the terms were unfavorable, or that there was disagreement with the valuation, as has been reported.

Additionally, the leaked document appears to contradict some of the information Mode communicated to employees on September 15, as the company was closing. According to a staff memo obtained by the Wall Street Journal, Mode told its employees that it had been “actively and continuously” searching for financing for the past five months. The memo also said, “We deeply regret having to take this action and we wish we could have provided you with greater notice.”

Yet the Mode board of directors had met a week earlier and voted to close the company and to deny funding for benefits like severance pay and COBRA health insurance. On September 9, three Burda-appointed directors approved the motion, according to sources. These directors were Martin Weiss, CEO of Burda Principal Investments; Andreas Rittstieg, head of Burda legal and compliance; and Jim McVeigh of investment advisory firm Cyndx. Burda did not immediately respond to a request for comment. McVeigh also declined to comment.

The unexpected action by Mode’s directors is hard to fathom. What was the financial motivation for taking such a drastic measure? Perhaps Mode should actually have shut down on September 10 if it were unable to meet its expenses. While startups may come and go in the blink of an eye, most investors prefer orderly wind-downs and seek to ensure that exiting employees receive benefits like COBRA insurance.

In the case of Mode, however, an assignment for benefit of creditors is already underway.

Here is a timeline of events surrounding the possible $10 million financing that might have saved Mode Media:

February 22, 2016: Then CFO Ernie Cicogna presents the PFG financing proposal to the board, which approves a motion to finalize and execute the financing agreement.

March 9: Final terms of the PFG financing are sent to the board (see cover sheet above).

March 31: Final terms and a draft of final documents of the PFG financing are discussed by the board, including those directors from Burda. A motion is put forth to enable Burda to gain control of Mode and to change the company’s management. Directors Andreessen, Arora, and Cicogna vote against the Burda plan. Weiss, Rittstieg, Efferen, and McVeigh vote in favor of the plan. The Burda faction prevails, even though it has only 38 percent of the company’s shares. Andreessen resigns as director.

April 1: Financing closing documents are delivered to Mode for execution.

Mid-April: Jack Rotolo is named CEO. Efferen resigns from the board. The board instructs CFO Cicogna to not close the $10 million financing round with PFG. Soon after, Cicogna resigns as CFO and as a director.

September 8-9: The board holds a two-day meeting in New York with Mode management (CEO Jack Rotolo and new CFO John Small) and Burda CEO Paul Kallen attending. On the 8th, Mode management presents a summary of company operations. On the 9th, directors Weiss, Rittstieg, and McVeigh approve a plan to shutter the company.

September 15: Mode Media closes.