Hollywood is the capital of movies, the Bay Area the capital of technology, Boston the capital of education and biotech, and New York the capital of the world. So, where is the capital of #insurtech?

Over the last two years, investment in insurance technology startups has multiplied, reaching $2.7 billion in 2015. As Matt Harris says, “in 2016 insurance feels like banking in 2009,” when a new breed of fintech startups — including LendingClub, Betterment, Transferwise, OnDeck, Robinhood, SigFig, Earnest, SoFi, and Stripe — started reinventing various areas of banking, creating value along the way.

Fintech and insurtech share many commonalities: They are part of financial services, are highly regulated industries, and are dominated by dozens of multibillion-dollar companies created more than 100 years ago. Insurance is a $1.3 trillion market in the US alone ($4 trillion worldwide). To put the size of the opportunity in perspective, as Spencer Lazar at General Catalyst Partners pointed out, this opportunity is bigger than the combined amount of money spent annually on online travel (~$160 billion), household work (~$460 billion) and food delivery (~$600 billion). Today, traditional insurance companies represent 10% of the Fortune 500 companies, and their average age is 95.

AI Weekly

The must-read newsletter for AI and Big Data industry written by Khari Johnson, Kyle Wiggers, and Seth Colaner.

Included with VentureBeat Insider and VentureBeat VIP memberships.

Insurtech startups are using data, design, and technology to compete with these juggernauts, usually innovating in one area of insurance, such as health, auto, home, or commercial. Many are focusing on one area of the value chain, such as underwriting (e.g., peer-to-peer, on-demand or based on new data models, and IoT) or innovative distribution models.

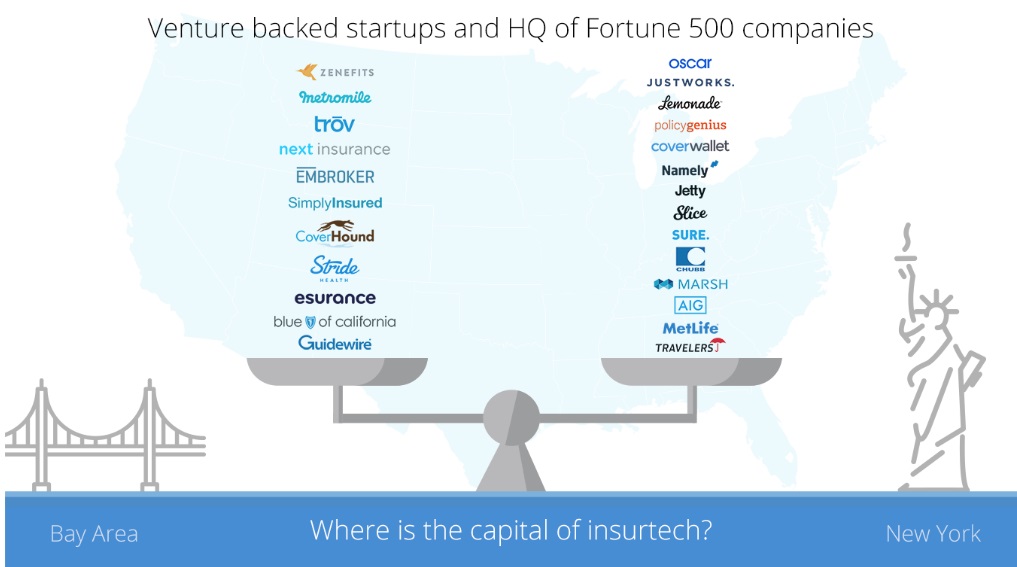

It comes as no surprise that most of these new insurtech startups are popping up in New York City, headquarters to some of the biggest insurance companies in the world, or in San Francisco’s Bay Area. New York is the home of most Fortune 500 insurance companies, including AIG, Metlife, Marsh, Chubb/ACE, New York Life, Teachers Insurance, Assurant, Travelers, VeriskAnalytics, and Alleghany. International insurance companies also have their US headquarters in New York, such as AXA, QBE, Prudential, Swiss Re, and Allianz. New York also has the advantage of being located just a few miles from Connecticut, headquarters of large insurance companies such as Aetna, Cigna, The Hartford, and W.R. Berkley.

Insurance is a highly regulated industry. You can choose to approach disruption from a naive point of view, but very quickly your startup will need to solve for regulation. Being close to sources of insurance domain talent can make the difference. Additionally, insurance is partnership- and business development–heavy, and from New York, you can take 30 key meetings in a week within a mile of your home or office.

On the other hand, sometimes, knowing too much about the industry can be limiting, making it hard to see things from the customer’s perspective and to sense how your product might simplify their lives (Paypal, Wealthfront, and Stripe have proven that). It is also very unlikely that you’ll find a combination of tech product and insurance expertise in an entrepreneur. So you need a city or an ecosystem that is a hotbed of tech/product entrepreneurs but is close to large insurance companies, so you can attract domain expertise, very early on, to compensate for the boldness and naivety.

Most of the venture-backed startups making the most noise in insurtech started in New York, such as Lemonade, which raised the largest seed round of the year from Sequoia before launching, and Oscar, which has raised close to $1 billion. Both companies were started by tech entrepreneurs with zero previous expertise in insurance, but very early on they complemented their skills with executives from the industry, recruited from companies that were less than a mile away.

However, the race is on to become the insurtech center of the world, as both San Francisco and Silicon Valley (the Bay Area) have also produced startups that are taking bold approaches to innovating insurance. Guidewire went public in 2012, with a pure software solution for the industry, and today is valued at $4 billion, and more recently, Zenefits and Trov have raised significant amounts of funding with innovative business models.

[aditude-amp id="medium1" targeting='{"env":"staging","page_type":"article","post_id":2028341,"post_type":"guest","post_chan":"none","tags":null,"ai":false,"category":"none","all_categories":"business,entrepreneur,","session":"A"}']

What makes a good insurtech ecosystem?

So, what makes for an optimal insurtech ecosystem? To be the capital of insurtech, a city needs to combine access to VC capital, insurance capital, and angel investors. You’ll also need access to insurance domain expertise at the executive level and individual contributors (otherwise you can get into trouble) and large insurance companies to partner with. You should also already have a number of venture-backed insurtech startups. And you should have access to universities, bold entrepreneurs, tech talent (e.g., digital marketing or UX/UI), incubators, and startups with executives who have experience scaling companies.

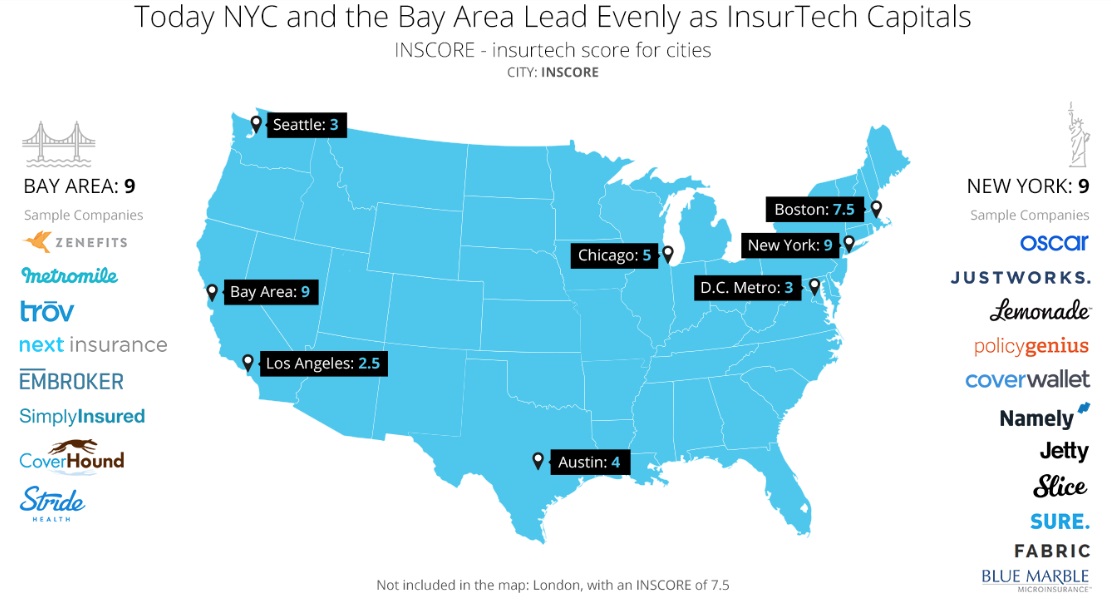

Based on the variables above, I have created my own score for the insurtech hubs, called INSCORE. (I’ve combined San Francisco and Silicon Valley into the Bay Area):

Here are some examples of insurtech startup in the most dominant cities:

[aditude-amp id="medium2" targeting='{"env":"staging","page_type":"article","post_id":2028341,"post_type":"guest","post_chan":"none","tags":null,"ai":false,"category":"none","all_categories":"business,entrepreneur,","session":"A"}']

- New York (INSCORE 9): Lemonade, PolicyGenius, Oscar, Namely, CoverWallet, Justworks, Slice, Jetty, Oscar, BlueMarble, Fabric, SureApp.

- Bay Area (INSCORE 9): Trov, Metromile, Coverhound, StrideHealth, NextInsurance, Embroker, SimplyInsured, Zenefits.

To be fair, New York and the Bay Area don’t hold a monopoly on Insurtech. Boston has a number of startups: Ensurify, MaxwellHealth, Goji, Quilt, FirstBest, InsuranceMenu, Enservio, Truemotion; and there are other promising startups around the country, including Insureon (Chicago), TheZebra (Austin), ImpactHealth (LA), or EagleView (Seattle). But I don’t think any of these cities will be able to challenge New York or the Bay Area for the title of head hub.

We’ll see more new insurtech startups launch in the next couple of years. I expect New York and the Bay Area to create more valuable companies — with entrepreneurs without insurance background, but who possess excellent data, design, and technology DNA. The Bay Area will probably generate more disruptive companies that will cover smaller niches. For other cities without tech entrepreneurship DNA, I think we will see insurance executives transitioning to tech entrepreneurship and building incremental innovation — but the companies that come out of that may create large valuations via profitable business development deals thanks to their former relationships in the industry.

Inaki Berenguer is CEO of online insurance startup CoverWallet, based in New York.

VentureBeat's mission is to be a digital town square for technical decision-makers to gain knowledge about transformative enterprise technology and transact. Learn More