The Facebook Messenger platform opens many doors for easier, better digital interactions by enabling businesses to embed codes in chat conversations. Businesses can now obtain user messages, translate them into action requests, and send back automatically generated or manually-typed-by-human responses to the users. This is a faster, simpler, and richer experience than mobile app interactions, which require users to navigate through a mobile app, click on different links, load new pages, and wait for confirmation.

The new Messenger platform will affect the banking industry significantly because most banking services are tasks that can be automated, and instructions can be provided in simple human language (e.g. “pay my Internet bill”).

Today, if I want to send money to someone, I must complete the following tasks:

- Open my banking app

- Login to my account

- Wait for authentication

- Navigate to Send Money

- Enter payee information, my account, and amount

- Submit request

- Confirm order

- Receive confirmation

There are usually a few seconds of wait time between each of these steps as new pages are loaded and I navigate to the right buttons in order to interact with the app.

With Facebook Messenger, I can just type “Send $200 to Jack Nielson” in a message to my bank. By looking at my list of payees, my bank will know who Jack Nielson is (if it doesn’t know, it can ask for more information) and which account the money is coming from (if it can’t decide, it can ask again). Of course, some technologies must be built to make sure that the correct action is taken upon receiving a user’s message, but such programming challenges will easily be overcome over time.

Chat bot applications for banking

Thanks to mobile banking and online banking, visiting a branch is no longer necessary for day-to-day banking. In fact, many digital banking startups feel there is no need for a branch-based business model and run their whole business on the web and mobile. Chat bots will help banks automate tasks further by making it seamless for the users to submit their inquiries.

Chat bots are also a great tool for the banks to simplify their digital interfaces, while being easier to maintain than an app. To support a new Messenger command (e.g. “what’s my credit card balance?”), there is no need for an app to be developed and published in the App Store. All the bank has to do is to write code that translates the message to a certain set of actions in the back end. Thanks to new solutions such as Facebook’s Artificial Intelligence and Microsoft Bot Platform, turning a message into a request is simple.

Here are some of the immediate applications of chat bots for banking.

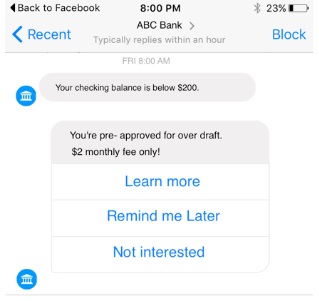

Alerts: Chat bots are great tools for delivering alerts to users’ accounts. You can get a quick sense of the experience by subscribing to CNN’s Messenger bot, a great alert tool that sends a summary of news items to subscribers every day. Banks can leverage the alerts capability to enable features such as “send daily account summary” or “low balance alert” for users.

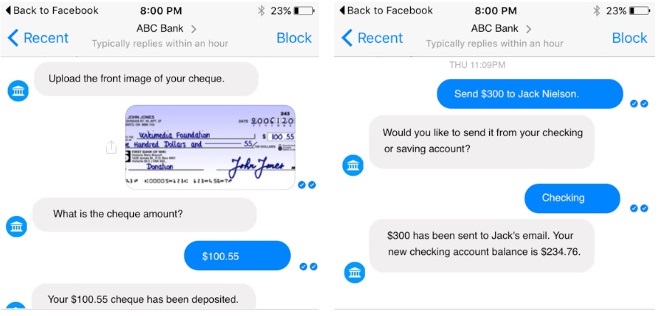

Day-to-day banking: Facebook users will soon be able to transfer money, pay bills, and deposit checks via Facebook Messenger. Creating a simple money transfer experience on Messenger will take some time. There will of course be challenges such as authentication, user mistakes, and privacy that must be addressed.

It is interesting to note that Microsoft has launched a Bot Framework that makes it easy for businesses to build a translation engine that translates user messages into actionable requests. Users will eventually be able to send a screenshot of a check to their bank, expecting that their bank will turn that image message into a money deposit request.

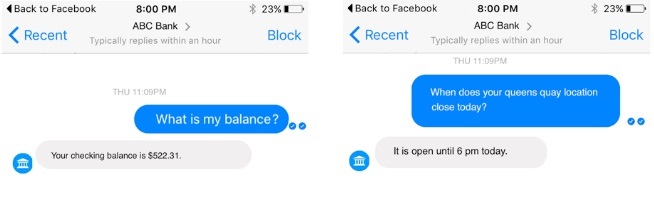

Inquiries: Instead of opening a banking app, users will find it more convenient to go to Facebook Messenger and ask questions such as “what’s my balance today?” It is also simpler for the bank to add support for new inquiries in Messenger than to support it by revising a mobile application. To support “what’s my balance today?” in Messenger, a bank doesn’t need to worry about UX, app development, managing mobile sessions, etc. All it needs to do is to act on the request and send an automatically generated response back to the user.

Search: Searching in Messenger will be radically different than searching in a browser. It’s a lot easier to type a question on Facebook Messenger than to go to a browser or a bank app. In addition, a user will always have access to previous inquires and can easily access them by scrolling up.

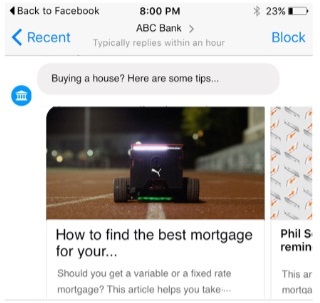

News and education: It hasn’t been easy for banks to develop a content delivery strategy for customers because financial education is not an interesting topic to a large segment of the public. Using chat bots, banks can push personalized financial educational content to any of their chat followers, including those who are not customers. Users can select their topics of interests and receive information that matches their needs. In addition, the bank can look at customers’ previous Messenger inquiries and optimize their personalized content accordingly. If a customer is asking questions about his or her balance, for example, a bank can send money management tips. If a customer is asking about mortgage rates, the bank can send content about buying a house and applying for a mortgage.

Customer support: It is more convenient for the average user to speak to a customer support agent on Facebook Messenger than on a private chat service on a website or an app. On Messenger, a user can post a question without giving it their full attention and come back to it at a later time to review the response. Users don’t need to wait for an agent to respond immediately.

Offers: Banks can present offers and promotions in Messenger. The offers can be personalized (e.g. “pay off your $2,000 credit card debt today”). There is also an almost 100% guarantee that customers will see these messages. After all, there is only one way for a customer to contact their bank – via Messenger.

These are just a few practical uses that highlight the importance of Facebook Messenger to the future of banking. It is crucial for banks to take advantage of Facebook Messenger if they wish to retain or increase market share.

How bots benefit banking

Some of the applications mentioned above have direct impacts for banking. Below are some of the more significant benefits.

Increased user engagement: With Messenger, it will become easier for users to engage with their banks. No more 1-800 calls with confusing automated menus, long wait times to speak to an agent, call center business hours, or delayed response times in chat rooms. There will now be fewer reasons for people to visit a branch, call customer support, or visit a website. Users will say and type what they need and will expect their bank to handle the rest. It is a pleasant experience for users to be able to connect with their bank anytime, anywhere, and without having to give full attention to the interaction.

Access to big data: Banks will be able to aggregate Messenger messages to learn significantly more about their customers. They can use conversation histories to offer more relevant content, offers, and automatically generated responses. After all, it is a lot easier to understand customers’ behavior and intentions by reading their requests in simple English than by analyzing clicks and navigation behavior.

Lower development costs: Supporting a new functionality on Facebook Messenger costs less than supporting a web or mobile interface. To launch a new feature for a web or mobile application, a significant amount of development, QA, and usability testing efforts are required to develop a user friendly interface. To support a new inquiry on chat bot, the bank simply has to develop the back office capabilities that support that request and set an automatically-generated response.

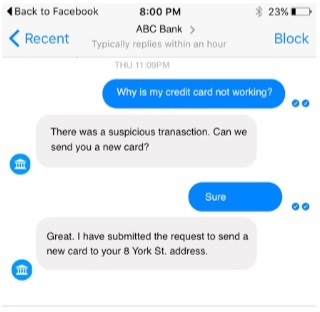

Reduced call center calls: Customers will no longer have to call for answers to their inquiries. They can just post their questions on Messenger. Imagine a user simply typing “my credit card is lost. Please cancel it,” instead of calling a 1-800 number and speaking to an agent.

Banks will discover many other benefits to supporting Messenger. It’s a path all banks will eventually take, just as they launched online banking and mobile banking.

Challenges with bots for banking

Although the benefits of chat bot banking are many, there are some risks that must be addressed.

Authentication: Facebook’s Messenger Platform V.1 does not currently offer an integrated authentication solution. If I message 1-800-Flowers, for instance, and ask to send roses to my wife, they will ask for my name and payment information because they don’t currently have a way of connecting my 1-800-Flowers account to my Facebook Messenger account.

This is a temporary limitation that will eventually be addressed by either Facebook allowing third parties to enable authentication inside their chat bots, or by the adoption of Facebook Connect by businesses. Facebook certainly prefers the latter approach, but many businesses, especially banks, will not be comfortable using Facebook Connect as an authentication solution due to fraud concerns.

I believe that Facebook will soon open the Messenger platform for third-party service authentication inside chats. The solution might be something as simple as contextual data (e.g. typing speed and pattern) or biometric authentication (e.g. Touch ID). In any case, a bridge will be built between Facebook accounts and businesses’ client profiles. Allowing businesses to complete their own authentication inside Messenger is certainly better for the banks as this approach eliminates the need to install Facebook Connect in their online banking systems.

User error: Typos can create frustration when using Messenger. Imagine if a customer enters an extra digit, or misses a digit in a money transfer request. There are a few UI solutions (e.g. requesting confirmation of amount) that can address these challenges, but it will take some time for the banks to optimize their Messenger interface to handle these scenarios.

What’s next for Messenger banking?

Due to the high scalability of Facebook Messenger, it is predicted that the adoption rate for Messenger bots will be much higher than any disruptive software or hardware device in the past. Bank of America has already announced plans to launch support for Messenger.

Given the importance of security and privacy in banking, it is essential for banks to start playing with chat bots as soon as possible. Due to the current limitations with authentication in Facebook Messenger, banks should begin by focusing on areas that do not need authentication, like search, news, education, and general inquiries. Phase 2 can include more complex services such as live chat and alerts. Phase 3 will include services such day-to-day banking in Messenger with secure authentication.

Bijan Shahrokhi is a product manager. He was one of the founders of Virtual Next, an app-free mobile payment and loyalty platform that uses Apple Wallet and Android Pay.