The usage-based insurance (UBI) model has been around for over a decade, but it finally started seeing traction in the past few years. EY, in a white paper that considers whether UBI is the new normal, reported that, as of July 2015, the Global UBI market adoption was less than one percent but that it is expected to grow to 15 percent in Europe, Asia, and America by 2020. In August 2015, Willis Tower Watson reported that millennials show particularly strong interest in a UBI policy — 88 percent “interested” or “maybe,” compared to 74 percent for other survey participants. With the current trends of the quantified self and quantified car, I can see insurance companies moving to appeal to millennials with a more data-driven model.

In June 2014, Frost and Sullivan forecast that OBD-II dongles would grow from a $160 million market to $1.6 billion in 2020, adding: “UBI has been the biggest driver for OBD-II based solutions thus far, and this trend will remain over the forecast period.” Now, two years later, there are a few standout dongle-based insurance companies, such as Metromile. But it looks like most of the major UBI programs in the U.S. are moving away from dongles and toward smartphone-based UBI apps. While we still have time before 2020 to see whether these market research forecasts pan out, let’s check in to see how the markets are swaying.

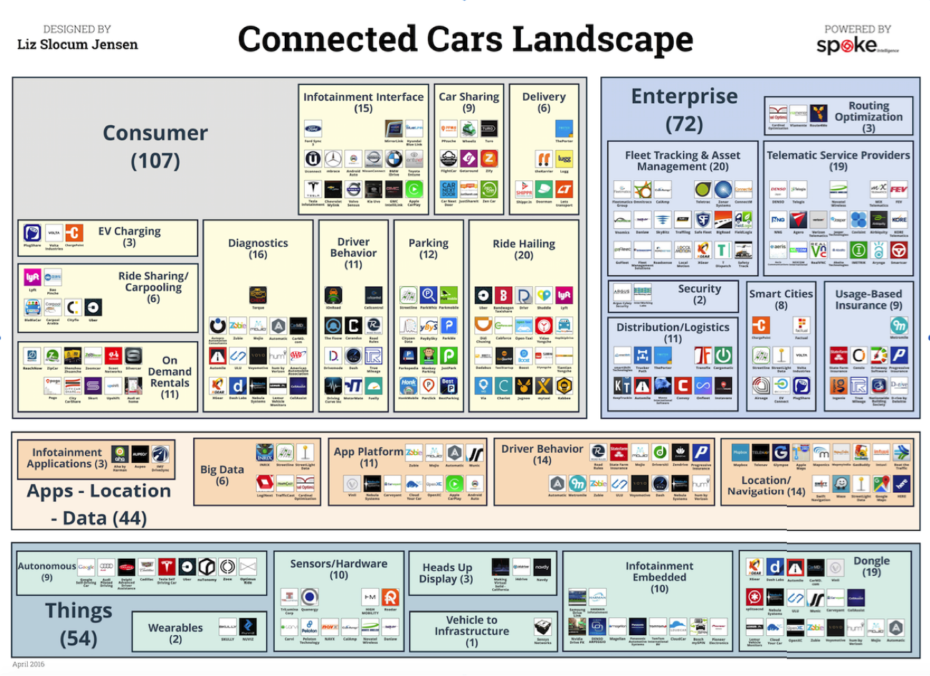

Above: VB Profiles Connected Cars Landscape. (Disclosure: VB Profiles is a cooperative effort between VentureBeat and Spoke Intelligence.)

This article is part of the Connected Car Landscape. You can download a high-resolution version of the landscape here.

Emergence of usage-based insurance

Progressive was one of the earlier adopters of UBI about a decade ago, with Snapshot, and it currently offers an ODB-II dongle-based plan. There are also a few white-label UBI solutions. Octo Telematics and TrueMileage provide dongle platforms to collect and report the data to unspecified insurance programs. Meanwhile, TrueMotion (formerly Censio) is betting on a phone-based UBI, supplying Progressive’s Snapshot mobile platform. State Farm is taking the anything-but-dongle approach in their Drive Safe & Save program that supports reporting via a mobile app, GM Onstar, Ford Sync, or self-reporting. Esurance is also migrating away from the dongle UBI format to a mobile app. There are even data exchanges being launched: Verisk Telematics Data Exchange and Octo Telematics, both of which aggregate connected car data to update insurance risk assessment models for a Pay-How-You-Drive format.

The trade-offs of mobile phone apps and dongles/telematics

Dongles come with a startup cost, and distributing the hardware creates a barrier to entry for the consumer. However, the trade-off in going with a mobile app UBI solution is that you compromise on accuracy in terms of the miles driven and even the driving behavior. As someone who built an app that uses the sensors on the smartphone to detect driving automatically, I know that there are a lot of challenges involved in making this work accurately. There will be inaccuracies, including, but not limited to, location, who’s driving, true driving status, verified driver behavior, activity, distance driven, and riding in a taxi/Uber/Lyft versus driving yourself. If you are getting the data directly through the telematics system via the OEM or a dongle, there will be better insight into the use of the insured vehicle. Linking the phone app to the car, either via the embedded telematics or an after-market dongle, is the best and most accurate way to detect and measure driving because the data is extracted directly from the CAN bus of the car.

How different is a system that incorporates telematics data?

Traditionally, auto insurance used aggregated historical data, including driving record, car type, location, and personal characteristics (age, gender, marital status) to calculate rates. Now that the insurance companies can extract more information about your driving habits (distance, speed, frequency), they can offer more personalized services and accurate pricing. They can also use this information to sell you other products and services. This has the potential to transform a service that is traditionally viewed as fixed cost to variable cost.

Of course, privacy concerns are a natural reaction to this new format, but, as the mobile phone, internet, and even customer loyalty card industries have demonstrated, people are willing to give up a little privacy to save money and to gain valuable services. EY claims that UBI providers suggest an effective solution that has the potential to reduce claims cost by 40 percent and reduce policy administration by 50 percent, leading to substantially reduced acquisition cost and price policies.

In 2015, Consumer Reports released the findings of a two-year study that analyzed more than 2 billion car insurance price quotes from more than 700 companies in all 33,419 general U.S. ZIP codes. It’s an eye-opening studying that debunked common myths/beliefs about insurance pricing. Two surprising factors Consumer Reports revealed about U.S. car insurance pricing are that premiums are based on (1) your credit (except in California, Hawaii, and Massachusetts, where this is prohibited) and (2) your likelihood to pay more out-of-pocket instead of filing a claim.

Combine this with Last Week Tonight with John Oliver‘s coverage of credit reports; which revealed that these reports are highly flawed: One in four reports had an error and one in 20 were seriously wrong. American consumers should be upset that their insurance pricing is based not on how they drive — but on a metric with flawed inputs. Now that these studies reveal how much consumers have been kept in the dark about pricing models, should we be surprised that Metromile is the only dongle that offers Pay-As-You-Drive? Because it is based on actual driving data, Metromile is a more transparent way to price coverage; the pricing is variable, but it’s predictable. If this is becoming the new normal, legacy insurance companies should be worried that their pricing model will no longer be acceptable.

Currently, it seems that the challenges and costs of implementing a more accurate telematics insurance solution have been outweighed by the ease of implementing a mobile app on a phone that the consumer already owns. However, the inaccuracies of the mobile app mean that the data won’t add as much value to the consumer nor to insurance companies, in terms of risk evaluation and efficient coverage. In its current state, data from UBI, sensors, dongles, and telematics offers little opportunity to save you money on your plan and, instead, simply gives insurance companies more insight into how to sell you things.

VentureBeat's mission is to be a digital town square for technical decision-makers to gain knowledge about transformative enterprise technology and transact. Learn More