Want smarter insights in your inbox? Sign up for our weekly newsletters to get only what matters to enterprise AI, data, and security leaders. Subscribe Now

When Samsung launched its mobile payment service last year, it entered a market that put it head to head with Apple and Google. The idea behind Samsung Pay was simple: to offer a secure and easy-to-use mobile payment service that lets consumers make purchases practically anywhere physical cards are accepted. But just how different is it from Apple Pay and Android Pay, two competing services created by their respective operating system manufacturers?

Today, the company announced the rollout of a new user interface and experience, as well as in-app support for a select set of ecommerce companies.

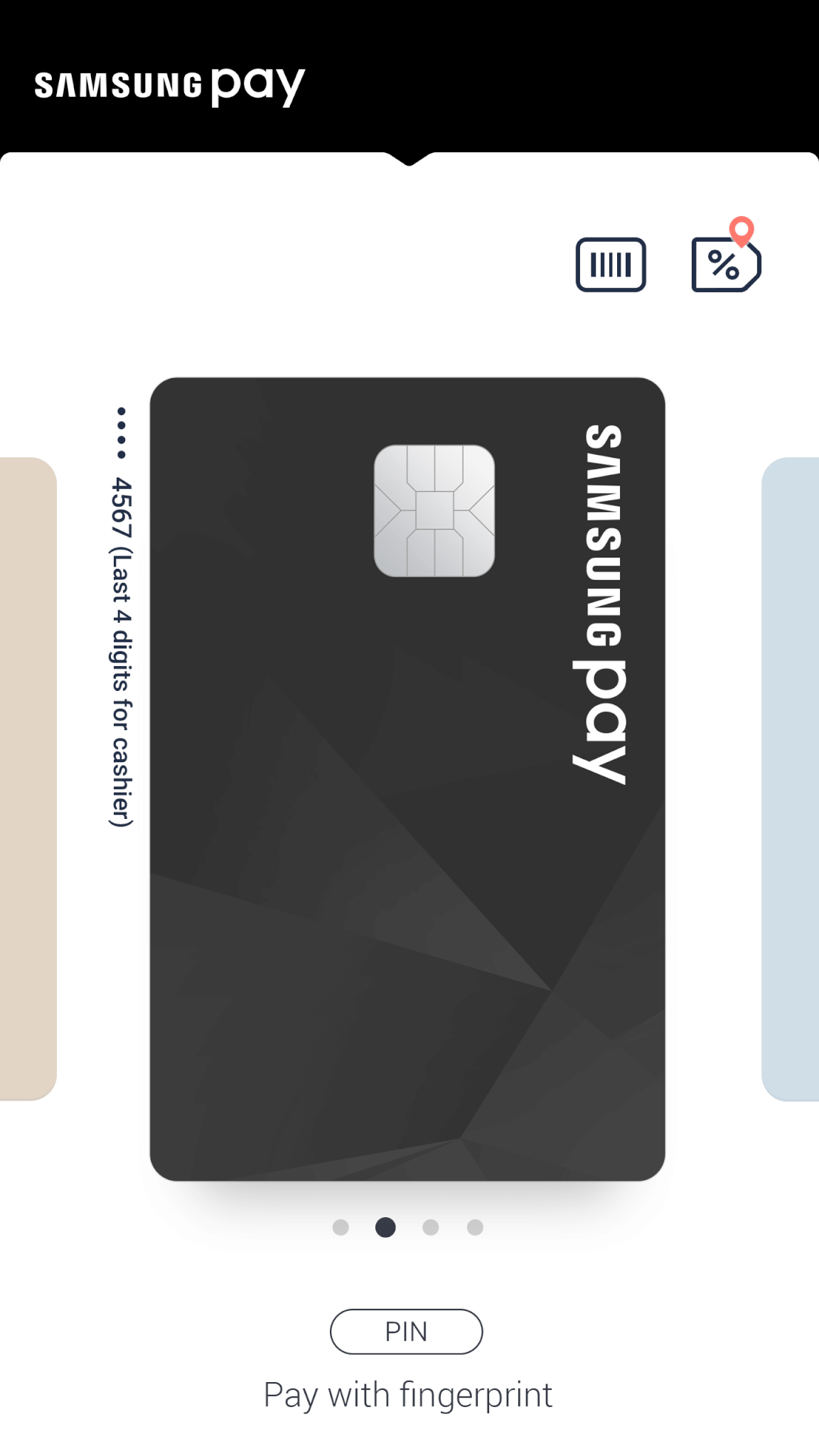

“If consumers always have to guess whether a store accepts a mobile payment, it creates a mental friction. I believe in creating a basic technology that removes that friction,” Samsung’s executive vice president, Injong Rhee, once said. It’s that type of thinking that has caused the electronics manufacturer to roll out a new user experience for Samsung Pay this year. It shifts the focus of the service away from being just about payments to becoming a true digital version of the wallet you carry around.

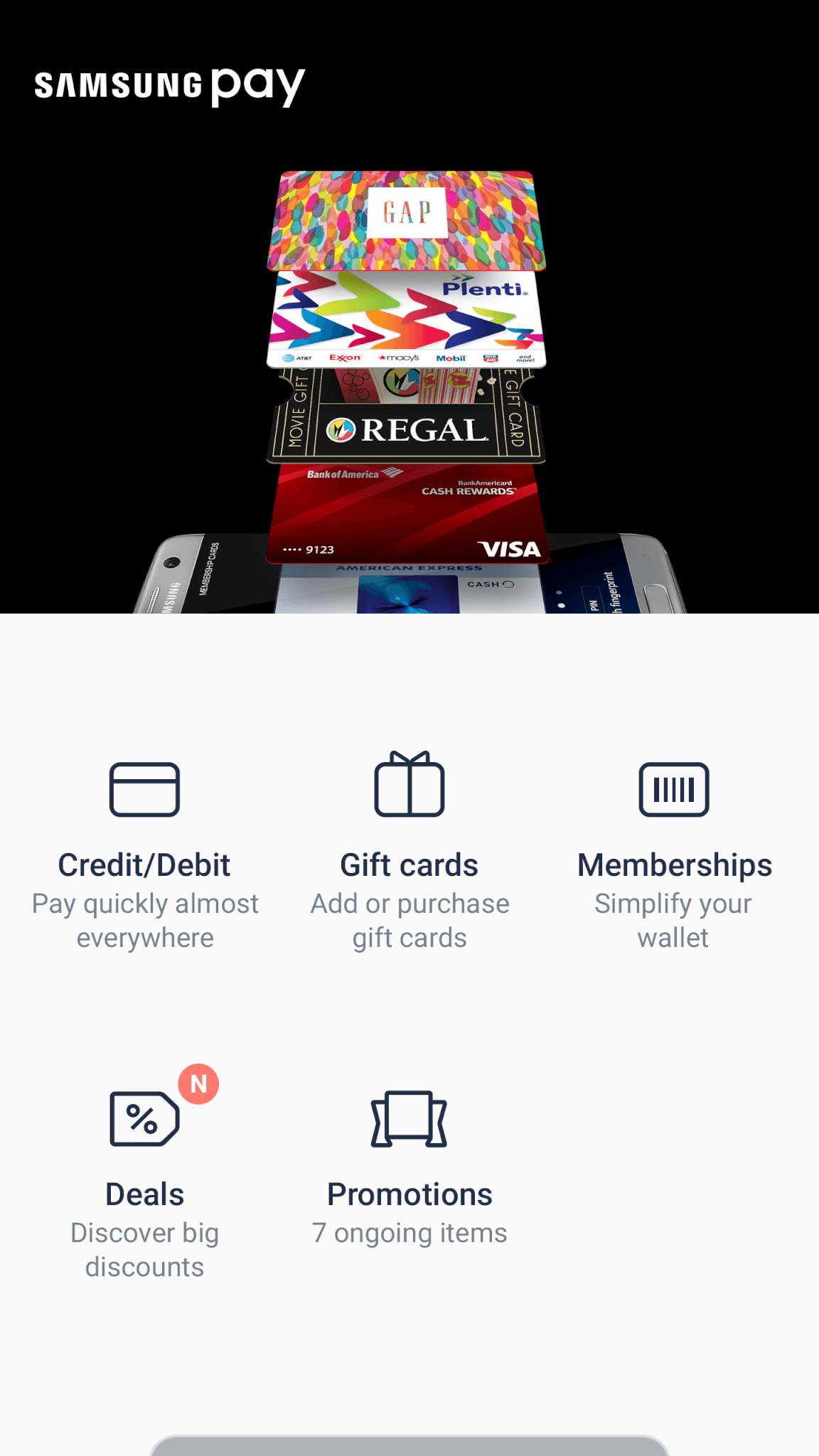

To give consumers a reason to switch from Android Pay or Apple Pay, Samsung is implementing its “payment+” strategy, which touts additional benefits for using Samsung Pay. Starting in November, the service has been transformed into something that’s the equivalent of Apple’s Passbook, where you can store digital versions of not only your debit and credit cards, but also of the 4 million membership and loyalty cards on the platform, like those for Safeway, CVS, Walgreens, Starbucks, Macy’s, and Sears.

This updated interface provides consumers with more use cases, but it’s also an opportunity to sell merchants on the idea that Samsung Pay is better than its competitors. Merchants can essentially craft a newsletter-like offering touting specials and providing relevant deals to customers, based on their location and other available and permitted data.

Samsung has even implemented some game mechanics, whereby select consumers receive coupons or other savings for actions such as sharing something on social media or making a certain number of transactions. Merchant promotions are not to be thought of as ad placements, according to Thomas Ko, the general manager for the company’s payment service, and can last between a few weeks and months.

“We decided that we’ll be more than payments,” Ko explained. “We wanted to be closer to the lifestyle of the user.” Beyond just being a place to store your cards, Samsung Pay will be a place to provide consumers with education on how to use the service, along with information about other Samsung offerings. Merchants can also purchase space to market their items and provide specials to consumers, based on location and interest.

While it’s one thing to facilitate mobile payments, it’s another to aid in discovery of relevant products. Of course, there are plenty of ways people can already make purchases, including with cash, credit or debit cards, checks, or digital offerings, such as the aforementioned PayPal, Apple Pay, and Android Pay, which just added support for Visa Checkout and Masterpass.

But Samsung thinks its advantage lies in how accessible it is. Peng Ning, the senior vice president at Samsung Research, shared that because Samsung Pay supports both Near Field Communication (NFC) and Magnetic Secure Transmission (MST), the service can be accepted by a majority of terminals, meaning that merchants don’t have to purchase additional hardware. To underscore the importance of this, just look at Mastercard’s announcement today that it has launched support for Samsung Pay, meaning that wherever Masterpass is accepted, Samsung Pay can be used. He also stated that users love the service, boasting that Samsung Pay has received the highest rating of any payment app.

While this payment experience is new to those in the U.S., it has been available in South Korea, where Ko stated users like the new offering and appreciate having a “slimmed down wallet.” But while South Korea’s version of this experience allows both online and offline purchases through Samsung Pay, promotions featured in the U.S. are limited to in-store offers.

A key indicator of a service’s potential is adoption, and, by all accounts, Samsung Pay seems to have some pretty good traction. It has enlisted the help of 500 banks worldwide and is now available in seven countries, with Malaysia, Thailand, and Russia to launch this year. The company reports that since Samsung Pay’s launch in South Korea, it has processed between $2 billion and $3 billion in transactions in the country. However, Ko said it was more difficult to assess total transaction volumes worldwide, due to data privacy restrictions imposed by individual banks.

Samsung also exploring native integration of Samsung Pay within apps outside of South Korea. This November, users will be able to use Samsung Pay as the default payment option within select merchant apps, starting with Raise, Fancy, Hello Vino, Wish, and Touch of Modern. While these are just the start of Samsung’s integration with third-party developers, there are other areas where this might come in handy. Ko said that the company wants to make sure that it’s available to all and that it will work openly with partners.

Of course, opening itself up to third-party developers requires some thought, which is why the company will be selective in which apps it works with. “Security is one of the most important things when it comes to payment and data,” Ko explained. “Samsung Pay is built on Knox; it’s the only one channel that [Samsung] controls. We will want to know who’s accessing our SDKs and APIs and certify that there’s no backdoor entrances.”